Introduction

This document focuses on the recent European Taxonomy regulatory framework. In particular, the goal is to examine the Green Asset Ratio (GAR) using the financial statements of the biggest European banks in order to understand how the European economy is transitioning in relation to the Taxonomy Regulation.

Starting from a high-level overview of the current situation, which allows us to understand the state of the art of the European landscape, we look at the main components in order to analyze the trends and to direct the analysis toward the importance of strategic policies and generation of sustainable services for the future of the European banking sector.

European Taxonomy Regulation

To support the transition path to a low-carbon economy, driven by the Paris Agreement on climate change and the UN 2030 Agenda, EU Regulation 2020/852 on the European Taxonomy came into force in June 2020, which is the first classification system that uses scientific criteria to identify the different economic activities carried out (or financed) as environmentally sustainable (according to the standards defined within the Climate Delegated Acts published by the European Commission).

As of January 1, 2024, Europe's largest banks are required to measure and report the GAR (Green Asset Ratio) in their Pillar 3 reports, or the proportion of taxonomy-aligned investments of the total assets.

An activity is considered aligned with the taxonomy if it makes a substantial contribution with respect to one of the six objectives under the EU regulation and, at the same time, does not significantly harm the remaining objectives (according to the so-called "Do No Significant Harm" or "DNSH" criterion). At the moment, alignment with the taxonomy is only reported with respect to the first two of the six objectives:

- Climate Change Adaptation (CCA), understood as the ability to predict and cope with the adverse effects of climate change;

- Climate Change Mitigation (CCM), defined as the ability to limit the impact of activities on the climate by reducing greenhouse gas emissions.

Assets considered in the calculation of the GAR numerator include:

- Exposures related to financial and non-financial corporations subject to disclosure under the Non-Financial Reporting Directive (2014/95/EU) (NFRD);

- Exposures related to loans and advances to individuals for real estate purposes and vehicle purchases.

The denominator also includes (in addition to the assets in the numerator) the bank's assets such as exposures to sovereigns, financing to SMEs and to non-EU entities.

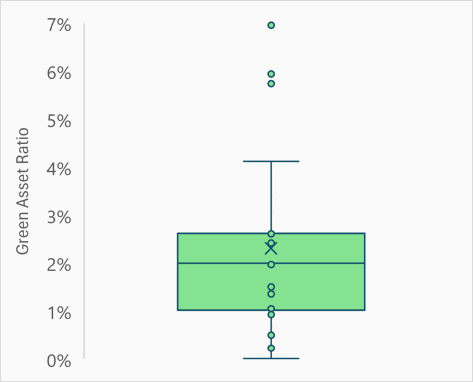

The first results declared in the Pillar 3 disclosure by major European banking groups[1] are shown in Figure 1, where Green Asset Ratio values are on average 2.4%.

Figure 2 shows, for each institution, the percentage of Taxonomy-eligible and Taxonomy-aligned assets based on the technical criteria dictated by the EU.

In this context, the heterogeneity of alignment and eligibility within the European framework can be seen, highlighting significant differences across financial institutions.

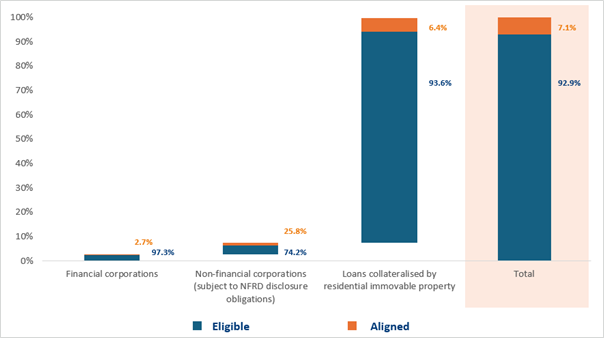

The analysis continues with consideration of the entire sample as a single bank, thereby combining the denominators, eligible assets and aligned assets of each institution into a single entity. Figure 3 shows which components contribute most to the percentage of eligible and aligned assets (GAR).

The graph illustrates the breakdown of eligible stock in the Total column across all banks under analysis. Indeed, the graph shows in the Total column the breakdown of eligible stock, shown in blue, and aligned stock, shown in orange, for all banks. The total is broken down into its primary components, comprising Financial Corporations, Non-Financial Corporations and Loans collateralized by residential immovable property[4].

GAR optimization tools

Figure 3 shows the key role of loans secured by residential real estate. On the one hand, they undoubtedly represent the largest component in terms of eligible assets, capable of having a very substantial impact on the total GAR; on the other hand, the share of aligned assets out of the eligible assets is relatively modest (6.4% percent versus, for example, 25.8% percent for non-financial corporation’s subject to NFRD). These characteristics make residential real estate-backed loans an attractive "lever" for investment to improve banks' overall GAR (and, with it, the public's perception of their ability to prioritize sustainable investments).

The low percentage of "aligned" residential properties[5] compared to the total eligible can be attributed to several factors:

- the absence of energy performance certificate information (in fact, only actual energy performance certificates acquired, rather than estimates, can be used);

- the exposure of the European banking system to properties that are not in the top 15 percent of the national housing stock in terms of primary energy requirements;

- the absence of timely physical risk assessments;

- the quality, granularity and availability of data on which to base the assessment (through a digitalization process that facilitates its use).

In order to extend the share of "aligned" properties, with positive effects on the overall GAR of banks, the following activities, primarily on new mortgages but also on the stock portfolio, can also be carried out:

- data remediation of building energy performance certificates through access to energy registries or contextually to real estate appraisals: this would meet the requirement of substantial contribution toward the taxonomy goal of climate change mitigation;

- more timely verification of the DNSH criterion with more detailed and granular analyses of physical hazard exposure, employing models that take into account the property's unique vulnerability to hazards. The analysis performed by CRIF and RED[6], in particular, demonstrated how property-specific vulnerability analysis raises the proportion of aligned properties by more than 10 percentage points[7].

Improving GAR through innovation and compliance

The European regulatory context is constantly being updated regarding energy transition and green directives; most recently, EU Directive 2024/1275 on the energy performance of buildings poses new challenges for the real estate market and the related financial market.

As seen in the previous analysis, the segment of loans on real estate assets is the main component of the share of eligible and aligned stock of the GAR. The strategic importance of this data is therefore fundamental for banks in order to understand which levers to apply to optimize Taxonomy alignment.

The data remediation of information from energy certificates and performance of physical risk assessments of the property therefore play a key role in optimizing the GAR.

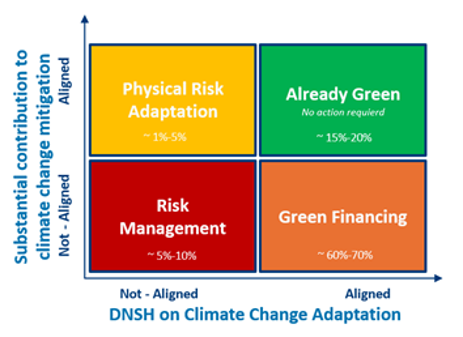

In addition to optimizing the GAR, this information also serves as a valuable business tool for banks. By analyzing a sample of over 10,000 taxonomy assessments conducted by CRIF and RED on residential properties, four main segments can be identified (Figure 4). Banks can implement risk mitigation and/or loan growth policies in these segments, thereby enabling significant business benefits.

Apart from the segment of properties that are Already Green, meaning those that are aligned with the European Taxonomy criteria based on the collected information, accounting for 15-20% of those analyzed, banks could implement the following strategic actions for the remaining portfolio:

- Risk Management: Properties in this segment (5%-10%) of the assessment sample have low energy efficiency and are significantly exposed to one or more climate-related and physical risks. The bank could put policies in place to mitigate credit risk.

- Green Financing (60%-70% of the assessment sample): This segment includes properties that are either moderately energy efficient (e.g., energy performance class “B” or “C”) or not energy efficient (e.g., energy performance class “C”), but that have low physical risk. In these situations, the bank could finance energy efficiency upgrades to raise the GAR and grow its business at the same time. The advantages will be even greater with the introduction of the new CRR (EU Regulation 575/2013), which requires the calculation of LTV based on the property value rather than the market value. If upgrades have been made to sufficiently increase the energy efficiency (i.e., sufficient enough to increase the energy performance class of the building to “A” or within the top 15 percent of the national housing stock by primary energy requirements), the property value may in fact be revised upward.

- Physical Risk Adaptation (1%-5% of the assessment sample): This category consists of energy-efficient properties that are nevertheless subject to one or more physical risks. In this case, the bank can increase the GAR and develop business by supporting the implementation of adaptation measures such as purchasing insurance policies, installing protective systems for windows and doors, inspecting and reinforcing the roof, etc.

These findings underscore the significance of a meticulous approach to securing the Energy Performance Certificate (EPC) and assessing physical risk as part of the credit approval procedure. This approach can effectively help banks gain significant advantages, including an optimized GAR, facilitated business development, and enhanced credit risk management. Additionally, this approach ensures compliance with European environmental sustainability standards.

[1] The sample of European banks analyzed consists of 20 significant institutions that have published a disclosure for the year 2023 with information about the GAR, with total assets ranging from €2,500 billion to €50 billion.

[2] The ‘×’ value represent the average GAR value in the system of the European banks analyzed.

[3] The values are ranked by the percentage alignment.

[4] The exposure component for the purpose of vehicle purchases, building renovations, local government financing and collateral obtained by taking possession is not included in the analysis as it is residual or zero.

[5] For example, for a building built before December 31, 2020, the property's alignment with the Taxonomy criteria for the climate change mitigation goal, according to the “acquisition and ownership of buildings” economic activity, is assessed by whether it has an energy performance class of "A" or falls within the top 15 percent of the national housing stock by primary energy requirements, and whether it is not exposed to significant physical risks according to DNSH compliance for the climate change adaptation goal.

[6] RED SPA is a highly specialized company which offers consulting services in the field of Risk Assessment for natural and man-made disasters.

[7] The outcome was achieved through a comparison of the alignment percentages derived from the CRIF-RED geographic physical risk scores and those linked to the CRIF-RED taxonomy alignment service, which also takes into account the building's technical and real estate attributes.